Double materiality is no longer just a “buzzword” in sustainability reporting — it’s the new compliance reality for companies under the European Sustainability Reporting Standards (ESRS). At its core, double materiality answers the question: “Material for whom?”

It requires companies to look at materiality from two perspectives:

- Financial Materiality – What impacts enterprise value and matters to investors.

- Impact Materiality – What impacts society, environment, and stakeholders beyond shareholders.

Together, they form the backbone of the Impacts, Risks & Opportunities (IRO) framework in ESRS and the Corporate Sustainability Reporting Directive (CSRD).

Key Insight:

- Finance-only reporting tells half the story.

- Impact materiality ensures that what matters to regulators, communities, and the environment is not ignored.

- ESRS revisions simplify disclosures but keep double materiality at the heart of compliance.

The Top 10 Mistakes Companies Make in Double Materiality Assessments

Despite growing awareness, many companies are still struggling with implementation. Based on EFRAG guidance and industry learnings, here are the most common pitfalls:

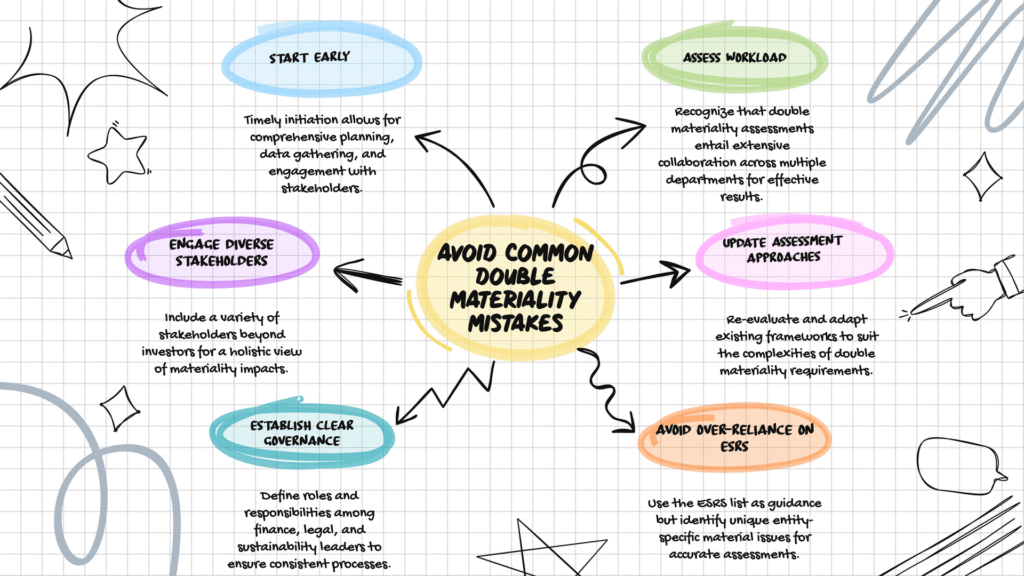

1. Starting Too Late

Many companies underestimate the sheer amount of work required. Waiting until the last minute leaves no time for proper planning, data collection, or engaging with key people inside and outside the company.

2. Underestimating the Workload

A double materiality assessment is not a simple checklist. It’s a comprehensive process that requires significant time, dedicated resources, and input from various departments beyond just the sustainability team. Companies that treat it as a side project will fall short.

3. Incomplete Stakeholder Engagement

It’s a mistake to only consult with obvious stakeholders like investors. The ESRS require companies to engage a broad range of affected stakeholders, including employees, local communities, customers, and even “silent stakeholders” like the environment, which may need to be represented by NGOs.

4. Relying on Old Approaches

Many companies try to adapt their pre-CSRD “single materiality” assessments. This is a pitfall because the new standards require a much deeper, more rigorous look at both financial risks and the company’s actual impacts on people and the planet, which may not have been considered before.

5. Lack of a Clear Plan and Governance

Without a clear roadmap and defined roles, the process becomes disorganized and inconsistent. It’s crucial to have a dedicated governance team with representatives from finance, legal, and sustainability to ensure the assessment is robust and auditable.

6. Over-relying on the ESRS Topic List

The list of sustainability topics in ESRS 1 is a starting point, not the end of the line. Companies must also identify and assess entity-specific topics that are unique to their business, sector, and operations.

7. Overlooking the Value Chain

A major challenge is assessing impacts, risks, and opportunities across the entire value chain—upstream (suppliers) and downstream (customers). It’s difficult to get the necessary data, especially from distant suppliers, leading companies to make unverified assumptions. EFRAG guidance acknowledges this, but companies still must make a good-faith effort.

8. Insufficient Documentation

The process must be transparent. Simply arriving at a list of material topics isn’t enough; companies must meticulously document how they identified, assessed, and scored each topic. Lack of proper documentation makes it impossible to justify decisions to auditors.

9. Treating Impact and Financial Materiality as Separate

While they are two distinct lenses, the ESRS emphasize their interlinkage. A social or environmental impact can become financially material over time. Companies that assess them in silos risk missing these crucial connections.

10. Aggregating Too Much or Too Little

Companies can get this wrong in two ways:

- Too much aggregation: Grouping too many issues together into a single, vague topic, which hides important details.

- Too little aggregation: Providing excessive detail on every minor issue, which makes the report unwieldy and hard for users to understand. The key is to find the right balance to provide a clear and concise report.

How ESGPro Mastery Institute Can Help

Navigating ESRS and CSRD requirements is complex. ESGPro Mastery Institute partners with companies to transform compliance into a competitive advantage by offering:

- ESRS Compliance Advisory – Align reporting with the latest EFRAG and ESRS requirements.

- CSRD-based Report Optimization – Craft reports that satisfy auditors, investors, and regulators.

- Double Materiality & IRO Workshops – Build internal capacity to conduct robust assessments.

- ESG Due Diligence – De-risk investments and strengthen financing opportunities by integrating ESG into corporate governance.

📩 Ready to future-proof your sustainability reporting?

Connect with ESGPro Mastery Institute today at esgpro.in to ensure your company doesn’t just comply — but leads. Write to us Now: info@esgpro.in

References

- EFRAG. European Sustainability Reporting Standards (ESRS) Implementation Guidance.

- European Commission. Corporate Sustainability Reporting Directive (CSRD).

- Global Reporting Initiative (GRI). Double Materiality & Impact Reporting Principles.